Can Unused Office Space Become Residential Real Estate?

Share this article

This article was originally published by Goldman Sachs Intelligence, a series featuring insights on diverse topics of impact within this dynamic economic environment.

As office vacancy rates rise in major US cities, and as residential real estate continues to be in short supply, the solution might seem obvious: turn office buildings into multifamily residences.

But even in this imbalanced market, there are large physical and financial hurdles to such conversions. Before the pandemic, only about 0.4% of office space was converted into multifamily units per year, and that figure has risen to 0.5% in 2023, Goldman Sachs Research economist Elsie Peng and analyst Vinay Viswanathan write in the team’s report.

“If you look at engineering reports and case studies, you see that converting large office buildings into smaller residential units is expensive,” Peng says. “You need to make a lot of adjustments, and the adjustment cost is very high.” If US cities are looking to solve their housing shortages through office conversion, government subsidies will be needed to make that feasible.

Goldman Sachs Research estimates that the annual conversion rate from office to multifamily will remain low and only increase to 0.6% in 2026, and to 0.7% in 2028. The conversion will create just 20,000 additional units for the multifamily market per year, a small amount compared to the 468,000 multifamily units that were built in 2023.

Too many offices, too few homes

The major post-pandemic trend in real estate is the rising vacancy rates in office buildings, as part of a shift to remote work. The office vacancy rate is 13.5%, the highest since 2000. “We expect it to rise even more in the next decade, because right now, a lot of office tenants are still locked into their contracts,” says Peng. “Their lower demand hasn’t been fully reflected in the vacancy rate yet. As their leases expire, the vacancy rates will rise.”

The increase in vacancies has led to office buildings across the US being rendered “nonviable.” Our analysts define this as a building that is more than 30 years old, that has seen no renovations since 2000, and that has a vacancy rate higher than 30%. Roughly 4% of offices in the US fit those criteria.

Share of nonviable office space in US cities

Source: CoStar, Goldman Sachs Research

An office is defined as nonviable if it is either in a suburban area or a central business district, was built before 1990, has not been renovated since 2000, and has a vacancy rate higher than 30%

At the same time, a supply shortage in residential housing has persisted since at least 2007. “The number of people aged 30-39 is the highest of any demographic in the country, and that’s typically when people move into their own places,” Viswanathan says. “So the demand for housing at this point is particularly high.”

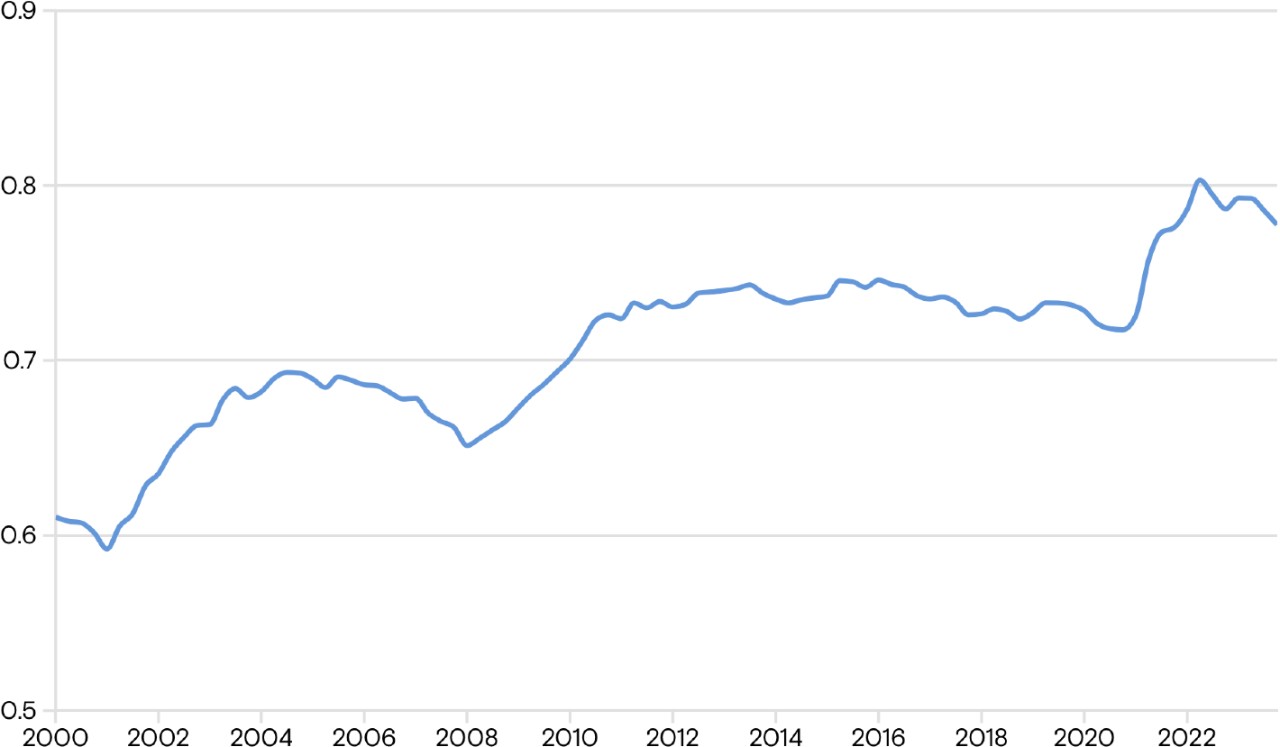

The rising returns for residential housing

Office space returns have dipped relative to multifamily rentals, as seen in the multifamily-to-office rent ratio

Source: CoStar, Goldman Sachs Research

The price is still too high to turn offices into homes

Converting underutilized office space to residential units is harder than it sounds — in large part because it’s expensive. The costs of acquiring and converting commercial buildings are high.

Prices also have not fallen to reflect vacancy rates, Viswanathan says. “Not many properties are changing hands, which is a function of the limited availability of financing, as regional banks are pulling back,” he says. “And banks, rather than liquidating defaulted loans, have been modifying them to give time to landlords to figure out their plans. So we aren’t seeing many foreclosure sales either."

The cost of regulation is also high. “Many cities don’t allow commercial buildings to be immediately used for residential purposes,” Peng says. “For developers to make that change could be a multi-year drag, which factors into their costs.” The team’s research indicates that only 0.8% of US office inventory is currently priced at a level that makes conversion to multifamily housing financially feasible.

This article is for informational purposes only and is not a substitute for individualized professional advice. Articles on this website were commissioned and approved by Marcus by Goldman Sachs®, but may not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions.

Related Content

4 min read

4 min read

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!